While the wholesale market will remain a key driver of prices, Ofgem's reforms and the introduction of new charges could raise costs further for households.

Dr Craig Lowrey Principal Consultant

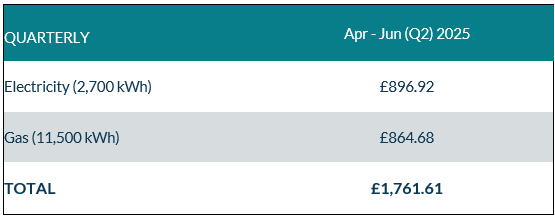

New forecasts from Cornwall Insight have seen price cap predictions rise to £1,762 a year for a typical dual fuel consumer1. This would represent a 1% increase from January’s price cap of £1,738 announced in November.

The increase in our cap forecast largely reflects the movement in the wholesale market, where economic and geopolitical factors affecting the global market have raised predictions for household bills. The continued uncertainty regarding the future of the Russia-Ukraine conflict and its implications for gas supplies to Europe is now occurring against the backdrop of an impending second Donald Trump presidency and its impact on gas exports from America – in addition to question marks over effects on economic growth in general.

We have also seen new information published on energy network charges and other non-wholesale costs, which is compounding the increase in the underlying costs of electricity and gas – all of which has caused the increase in our forecast.

In addition, there is also the prospect of reforms adding extra costs to the cap, which would represent at least another £20 on annual bills.

These potential reforms, which could take effect from April, include incorporating allowances to fund the Energy-Intensive Industry (EIIs) network charge exemption scheme - the scheme introduced through government legislation – which will compensate EIIs for a portion of their network charging costs. There is also a potential extension by Ofgem of the existing Supplier Bad Debt Allowance, which was introduced last year to cover additional support credit for some prepayment meter customers.

Factoring in the proposed reforms, our forecasts show the cap could rise to around £1,782, which would represent a 2.5% increase from January.

Looking further ahead, current forecasts suggest a drop in energy prices this July. However, we do not currently know the long-term impact of the recently announced extensions of nuclear plants - Torness in East Lothian and Heysham 2 in Lancashire to 2030, along with Hartlepool and Heysham 1 to 2027 – on wholesale prices, and therefore household bills.

Figure 1: Cornwall Insight’s Default Tariff Cap forecast using new Typical Domestic Consumption Values (dual fuel, direct debit customer) – without potential Ofgem reforms

Source: Cornwall Insight

Note: The figures do not include potential reforms which could add more than £20 to the price cap forecast.

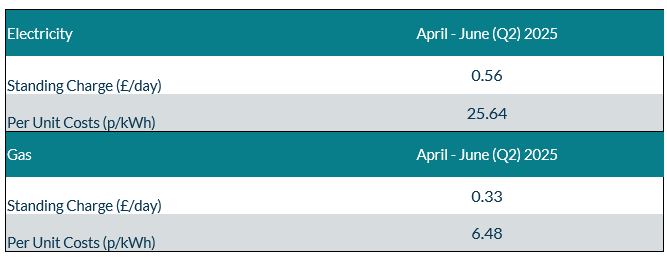

Figure 2: Default Tariff Cap forecast, Per Unit Costs and Standing Charge (dual fuel, direct debit customer)

Source: Cornwall Insight

Note: All figures are national average unless otherwise stated. All intermediate and final calculations are rounded to two decimal places. Totals may not add due to rounding.

Dr Craig Lowrey, Principal Consultant at Cornwall Insight:

Energy bills in 2025 are shaping up to reflect a perfect storm of regulatory changes and market turbulence, in addition to any broader sector reforms put forward by the new Government. While the wholesale market will remain a key driver of prices, Ofgem's reforms and the introduction of new charges could raise costs further for households. There are a lot of unknowns, and while significant rises in price are currently unlikely, the scale of any increases will depend on how the market and the reforms unfold.

What we do know is that the market is unlikely to lower bills, and affordability and fuel poverty will continue to be a pressing issue. This underscores the need for policymakers and suppliers to prioritise supporting vulnerable consumers. This could involve looking at short-term financial assistance, while simultaneously, focusing on longer-term solutions, such as reforming energy tariffs, accelerating energy efficiency programs, and investing in sustainable energy.

Reference:

- Ofgem’s Typical Domestic Consumption Values (TDCVs), are set at 2,700 kWh per annum for electricity, and 11,500 kWh per annum for gas.