Meeting the UK’s targets of a clean power sector by 2030 and a net zero economy by 2050 will require a significant growth in intermittent renewable generation, and an accompanying increase in technologies that can provide system flexibility – of which batteries are a key component. However, incentivising development of and investment in battery assets has been challenged by the revenue rollercoaster that batteries have experienced in the last few years, with highs in 2022 followed by lows in early 2024, before a recent resurgence in late 2024 and early 2025. Our BESS Analytics service, combined with ourFlexibility Markets Hub, allows these trends to be interrogated to identify their key drivers and help understand the impacts of these drivers on the evolution of the GB battery revenue stack.

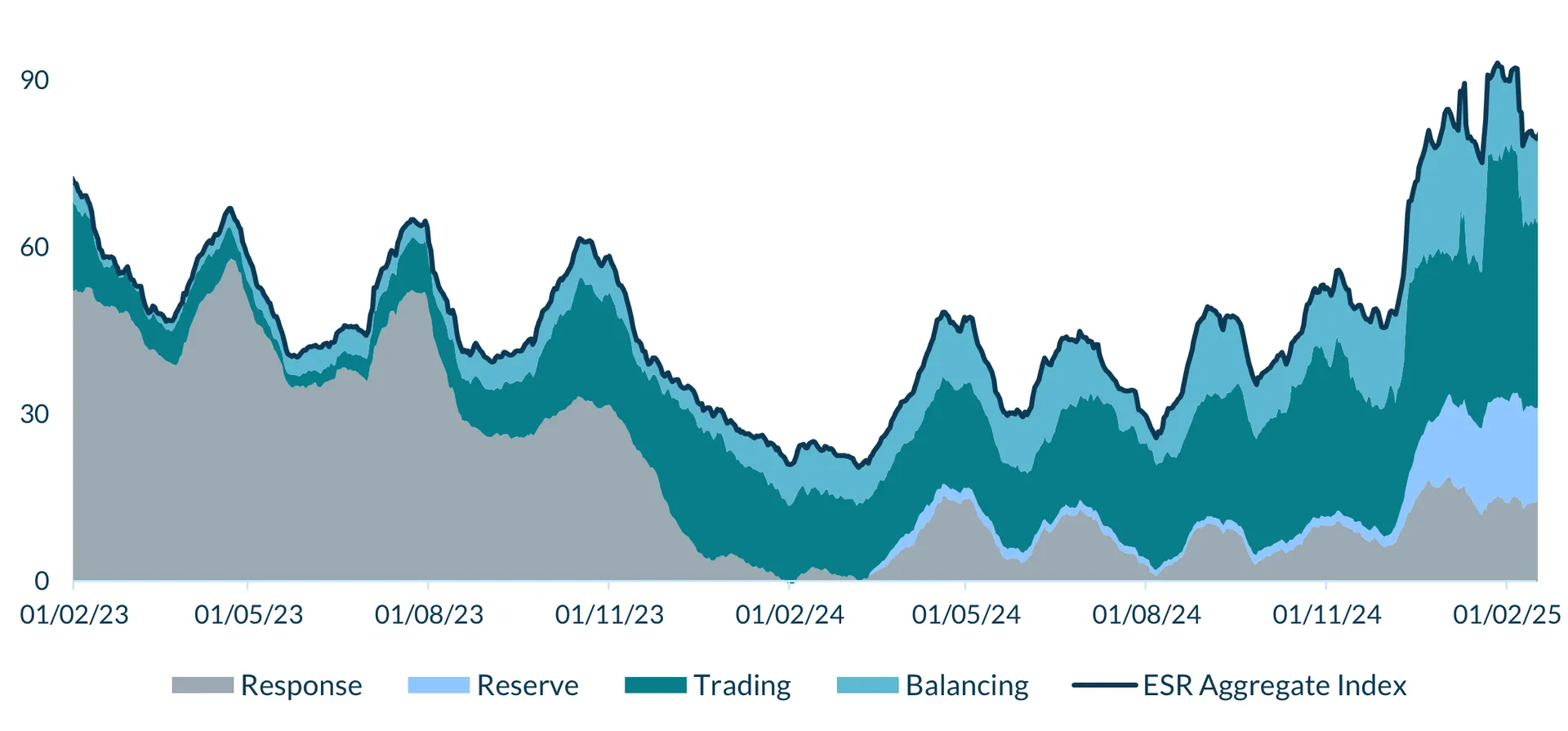

Throughout 2024, and into early 2025, there has been a marked shift in the revenue stack for battery assets (Figure 1) away from one dominated by response services to a more diverse trading portfolio underpinned by wholesale trading.

Figure 1: Energy Storage Revenue Index (30 day rolling average, £’000/MW/yr) January 2023 – February 2025

Source: Cornwall Insight – BESS Analytics

This diversification, alongside broader market reforms has resulted in the revenue growth seen since December 2024:

-

Wholesale price spreads and negative pricing. Tight system margins and increased price spreads during January 2025 provided greater arbitraging opportunities for battery assets. Negative pricing periods have also seen an increase throughout 2024, nominally increasing achievable price spreads for batteries. Although, this opportunity has been limited by the concentration of 41% (63 hours) of the negative price periods within only five days.

-

Introduction of Quick Reserve. Since the introduction of Quick Reserve, a new frequency management tool from the National Energy System Operator, in December 2024, the service has seen fairly lucrative returns for battery assets (£8.75/MW/hr for Positive Quick Reserve and £5.12/MW/hr for Negative Quick Reserve). This has seen reserve services grow from a relatively minor component of the revenue stack at the beginning of the winter to now accounting for ~20% of battery revenues. However, with our BESS Analytics project pipeline indicating that another ~6GW of batteries are due to come online by the end of 2025, it is possible that the healthy returns seen so far from Quick Reserve could follow a similar pattern to the other frequency response markets, with market saturation dampening revenues.

-

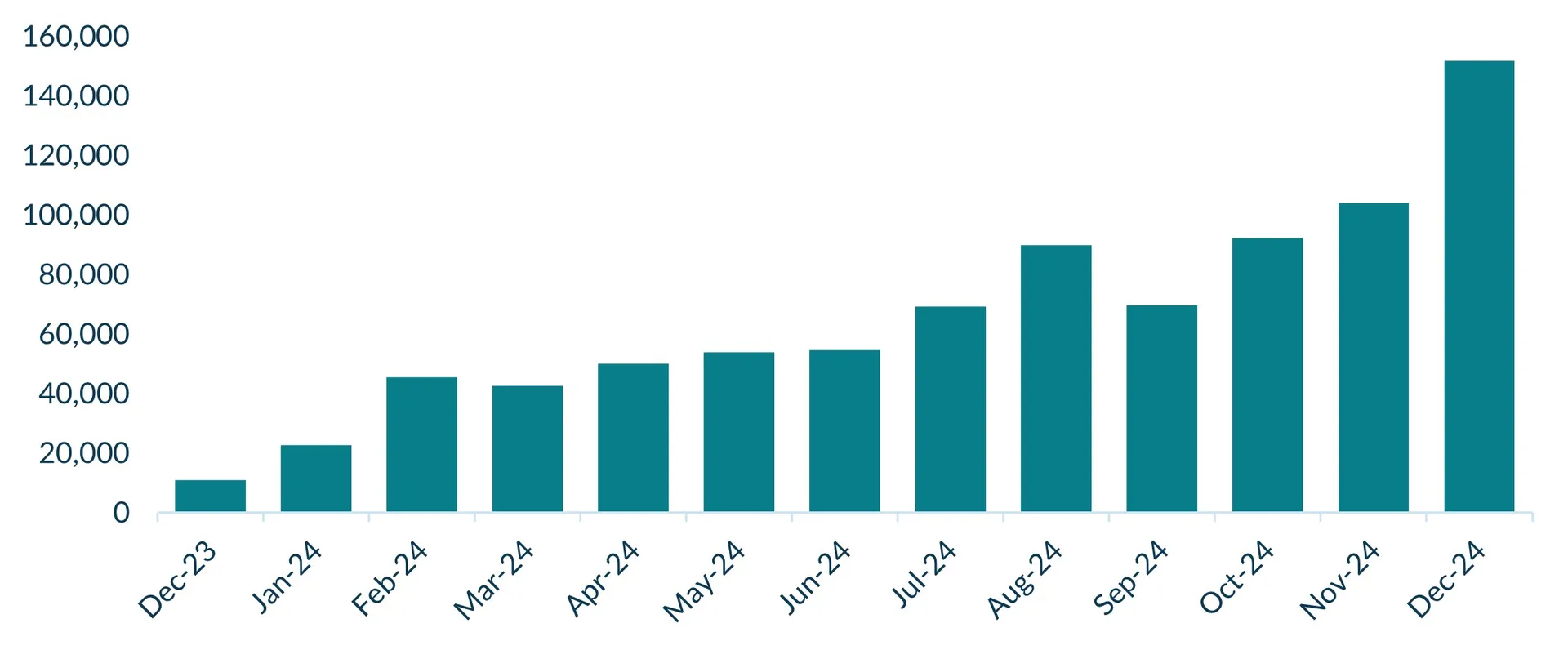

Evolution of the Balancing Mechanism (BM). Since the launch of the Open Balancing Platform (OBP) in December 2023, skip rates of batteries in the BM have been reduced, with an ever growing number of battery BM Units being dispatched each month across 2024 (Figure 2). This is just part of a series of reforms and improvements aimed at allowing more efficient dispatch of batteries in the BM.

Figure 2: Monthly number of battery dispatches in the BM December 2023 – December 2024

Source: Cornwall Insight – Flexibility Markets Hub

Alongside the broad changes in the battery revenue stack over the last year and into the future there has also been an evolution in routes to market with growing interest in tolling agreements or flexible power purchase agreements with floor prices.

Looking to the future, while exact trading strategies and revenue stacks will vary on an asset-by-asset basis, GB batteries are forecast to secure the majority of their revenues from wholesale arbitrage and the BM. It is, however, clear from the detailed breakdown of different asset routes to market in our BESS Analytics service that there is no one-size-fits-all solution to battery trading and operation. Overall, our latest GB Battery Revenue Forecast indicates that the general outlook for batteries is positive out to 2040.

Interested in our comprehensive BESS Analytics service? Get end-to-end insight, analysis, and forecasting across all the major revenue streams for flexible assets in GB, find out more here. For a copy of the full Insight Paper, contact Peter Carr at p.carr@cornwall-insight.com .

If you are a customer, you can find the full Insight Paper in the Thought Leadership section of CATALYST.